An AI-Generated Panel discusses Bitcoin

In this unique thought experiment, we leverage artificial intelligence to explore Bitcoin’s value proposition, risks, and future potential through the perspectives of four influential figures in finance and technology. By simulating their viewpoints based on their known positions and expertise, we can better understand the various arguments surrounding Bitcoin’s role in the future of finance.

Our Panel of Experts

Anthropic’s Claude Sonnet 3.5 was used to generate responses using the information the model has on the following Bitcoin, Financial and Economic experts.

Andreas Antonopoulos: A prominent Bitcoin advocate, educator, and author of several books on cryptocurrency. As one of Bitcoin’s most prominent advocates and educators, Antonopoulos has dedicated his career to explaining and promoting Bitcoin’s technological and economic significance. He’s written multiple books on the subject and is known for his deep technical understanding and passionate advocacy.

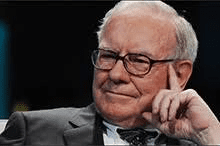

Warren Buffett: Legendary investor and CEO of Berkshire Hathaway, known Bitcoin skeptic. Buffett has famously called Bitcoin “rat poison squared” and has consistently criticized it as having no intrinsic value. He maintains that it doesn’t produce anything and its value relies solely on finding someone else willing to pay more for it.

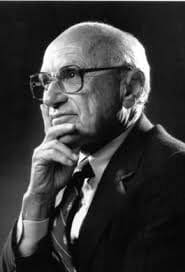

Milton Friedman: Nobel Prize-winning economist and free-market advocate. Although Friedman passed away before Bitcoin’s creation, his views on monetary policy, government intervention, and free markets suggest he would likely support Bitcoin. He actually predicted something like Bitcoin in 1999 when he spoke about the need for a reliable e-cash method on the internet.

Adam Back: Creator of HashCash and CEO of Blockstream, a pioneer in cryptocurrency technology. As the inventor of Hashcash (which Bitcoin’s proof-of-work system is based on) and the CEO of Blockstream, Back is one of Bitcoin’s earliest technical contributors and strongest advocates. He’s dedicated much of his career to cryptocurrency development and Bitcoin’s success.

Key Questions Explored

The AI Panel was prompted with each of the following questions.

- Does Bitcoin have any value whatsoever? If so, why?

- How do we value Bitcoin in US Dollars?

- What are the risks of centralized control?

- What could cause Bitcoin to become worthless?

- When will Bitcoin’s price stabilize?

- How do Bitcoin, Smart Contracts, and Stablecoins interact?

- What does the future hold for Bitcoin and finance?

Does Bitcoin have any value whatsoever? If so why?

Andreas Antonopoulos: “Bitcoin absolutely has value, and its value stems from multiple fundamental properties. First, it’s the world’s first truly scarce digital asset – you can’t just copy it like other digital items. Second, it’s programmable money that operates on a trustless, decentralized network. The value comes from its network effect, security through proof-of-work, and its ability to provide financial sovereignty. Most importantly, it enables people to store and transfer value without permission from any government or financial institution. This is revolutionary and has immense value for human freedom.”

Warren Buffett: “No, Bitcoin has no intrinsic value whatsoever. Unlike productive assets like farmland, companies, or even apartment buildings that generate products or services, Bitcoin produces nothing. It’s merely a speculative instrument that relies on the ‘greater fool theory’ – hoping someone else will pay more for it later. When I look at an asset, I ask ‘what does it create?’ Bitcoin creates nothing. It just sits there. You can stare at it all day, and no little Bitcoins come out or anything like that.”

Milton Friedman: “While I approach this from a theoretical perspective, I would say yes, Bitcoin has value. Its value derives from its ability to serve as a medium of exchange while being independent of government control. I’ve long argued that monetary policy should not be in the hands of central banks, and Bitcoin provides a fascinating free-market alternative. Its fixed supply schedule and resistance to manipulation make it potentially superior to fiat currencies in terms of maintaining stable purchasing power over time.”

Adam Back: “Absolutely Bitcoin has value. As someone who worked on digital cash problems for decades, I can tell you Bitcoin solved the double-spending problem in a truly decentralized way – something we never achieved before. Its value comes from its proven security model, decentralized nature, and fixed supply. The network has been running uninterrupted for over a decade, securing hundreds of billions in value. The computational power securing Bitcoin makes it the most secure financial network ever created. Its value is intrinsic to its technical properties and the security guarantees it provides.”

Question 2. How do we value a a Bitcoin or 100M Satoshis in US Dollars? For example if one Bitcoin is one dollar how do we arrive at that price? If I am paying for one Bitcoin how do I know I am paying a fair price? If I am selling a bitcoin how do I know if I am getting a fair bid?

Andreas Antonopoulos: “The price of Bitcoin emerges from an open, global market operating 24/7. But you’re asking a deeper question about fundamental value. Bitcoin’s price is determined by its utility as a network and its monetary properties. Think of it like valuing the internet itself – impossible in the early days, but the network effect creates massive value. Key metrics to consider are: network security (hashrate), number of active users, transaction volume, and adoption rate. The fair price emerges from market consensus across all global exchanges. As for determining a fair price when trading, look at the order books across major exchanges, consider the network’s fundamental metrics, and understand that Bitcoin trades against every major currency, creating a highly efficient global price discovery mechanism.”

Warren Buffett: “That’s precisely the problem – you can’t value Bitcoin using any rational method. When I value a business, I look at cash flows, assets, competitive advantages, and management quality. With Bitcoin, there are no cash flows, no assets, nothing to analyze. The price is pure speculation. People buy it at $10 hoping to sell it at $100, others buy at $1000 hoping to sell at $10,000. It’s a trading sardine, not an eating sardine. There is no ‘fair’ price because there’s no underlying value to measure it against. It’s worth what the next person will pay, nothing more.”

Milton Friedman: “The valuation question is fascinating from a monetary theory perspective. Bitcoin’s value, like any currency, derives from its utility as a medium of exchange and store of value. The key difference is its fixed supply schedule. In theory, as adoption increases, each unit should command more purchasing power, unlike fiat currencies which tend to depreciate through inflation. The ‘fair’ price would be a function of: total monetary value seeking a inflation-resistant store of value, divided by Bitcoin’s fixed supply, multiplied by Bitcoin’s probability of successful long-term adoption. But markets determine this price through countless individual decisions.”

Adam Back: “From a technical perspective, we can look at the cost of production through mining as a price floor – the electricity and hardware costs to produce one Bitcoin. But that’s just the minimum. The real valuation comes from Bitcoin’s utility as programmable digital gold. Consider: security budget (hashrate), network effect (users/transactions), and supply dynamics (halving schedule). For trading, look at high-quality exchanges with deep liquidity, consider macro factors like monetary policy, and remember that Bitcoin trades globally 24/7. The fair price emerges from this global market, but long-term value comes from Bitcoin’s fundamental properties as the most secure and decentralized monetary network ever created.”

Question 3. What is the risk that a foreign government controls the majority of the mining or the majority of the nodes thereby Bitcoin is no longer “decentralized” it is now mostly under the operation of a singular foreign entity?

Andreas Antonopoulos: “This is a common concern that misunderstands Bitcoin’s game theory and security model. Even if a single entity controls 51% of mining power, they can’t change the fundamental rules of Bitcoin – they can’t steal coins, create coins out of thin air, or change the 21 million supply cap. At worst, they could attempt to reorganize recent transactions, but this would be incredibly expensive and would immediately devalue their own mining investment. As for nodes, mining concentration doesn’t equal network control. Full nodes enforce the rules, and they’re distributed globally. Any attempt to change the rules would result in those nodes rejecting invalid blocks, regardless of hashpower. Plus, the beauty of proof-of-work is that it’s instantly relocatable – if one jurisdiction becomes hostile, miners can and will move elsewhere, as we saw with the China mining ban.”

Warren Buffett: “This risk just highlights another fundamental problem with Bitcoin. The fact that one foreign power – likely China or Russia – could potentially gain control over this supposed ‘currency’ is deeply concerning. We already know most mining happens outside the US. Why would any sensible investor or business put their trust and capital into a system that could be compromised by foreign actors? At least with the US dollar, we have a known entity – the Federal Reserve – and a government backed by the world’s strongest military and economy. With Bitcoin, you’re putting your faith in anonymous miners, many operating under potentially hostile foreign governments.”

Milton Friedman: “From an economic perspective, this concern actually demonstrates the robustness of Bitcoin’s incentive structure. Any entity gaining majority control would face a significant economic dilemma: they could either maintain the network’s integrity and profit from their investment, or attempt to destroy it and lose their entire investment. The free market creates a natural equilibrium here. If mining concentration becomes too centralized in one jurisdiction, the perceived risk would lower Bitcoin’s value, making mining less profitable and naturally encouraging geographic distribution. It’s a self-correcting system driven by market forces, which is precisely why it’s so resilient.”

Adam Back: “Let me address this from a technical perspective. First, mining and node decentralization are different issues. Mining is naturally driven toward cheap energy sources, but this doesn’t equate to control. The Bitcoin network is designed so that miners must follow the rules that full nodes enforce. Even with majority hashpower, a malicious actor cannot change Bitcoin’s consensus rules – they can only attempt to reorganize recent transactions at enormous cost. The node network is highly distributed globally, and this is what really matters for decentralization. Furthermore, developments like Stratum V2 and improvements in mining pool protocols are making mining more decentralized. The network has already demonstrated its resilience to geographic concentration when it survived and thrived after the China mining ban.”

Question 4. When you think about what would cause Bitcoin to become worthless for Bitcoin go from its current market price of $100,000.00 to $0.00, to nothing. What is the biggest risk, what is most likely to cause such an event?

Andreas Antonopoulos: “The only realistic scenario that could drive Bitcoin to absolute zero would be a catastrophic technical failure in its cryptographic foundations – specifically, if SHA-256 or elliptic curve cryptography were broken by quantum computing breakthroughs. However, the Bitcoin community would likely implement quantum-resistant algorithms before this becomes a real threat. Other scenarios like government bans or competing cryptocurrencies might reduce Bitcoin’s value but wouldn’t drive it to zero because Bitcoin’s core value proposition is its censorship resistance and network effect. Even during total internet blackouts, Bitcoin’s network can survive through satellite and mesh networks. The protocol’s antifragility means that most attacks only serve to make it stronger.”

Warren Buffett: “The most likely scenario is simply that people finally realize there’s no there there. Bitcoin’s value is built entirely on belief – belief that someone else will pay more for it later. Once that belief evaporates, so does the value. We’ve seen this pattern throughout history with various manias. Look at tulip bulbs in Holland – they went from being worth the price of houses to practically nothing when people came to their senses. Bitcoin doesn’t need a technical failure to go to zero; it just needs people to stop believing in the story. And when governments seriously regulate cryptocurrencies or launch their own digital currencies, that could be the catalyst that bursts this bubble.”

Milton Friedman: “From an economic perspective, Bitcoin’s value could theoretically approach zero if a superior free-market monetary alternative emerges that better serves the market’s needs. However, network effects are powerful – just as English remains the global business language despite its inefficiencies. The more likely risk is government intervention – not through direct bans, which would be difficult to enforce, but through regulatory frameworks that sufficiently restrict Bitcoin’s utility as a medium of exchange. If governments collectively make it too difficult to convert Bitcoin to and from traditional financial systems, its practical utility could be severely compromised.”

Adam Back: “As someone deeply familiar with Bitcoin’s technical architecture, I see very few plausible paths to zero. The most severe would be a fundamental cryptographic break, but Bitcoin can be upgraded to address such threats. Some worry about quantum computing, but we have quantum-resistant algorithms ready to deploy if needed. Government bans might cause price drops but wouldn’t drive Bitcoin to zero – it was designed specifically to resist state control. Even a serious bug like an inflation vulnerability would likely be caught by the thousands of eyes reviewing the code and could be fixed with a soft fork. Bitcoin has survived numerous challenges already – exchange hacks, the Mt. Gox collapse, chain splits, and more. Each challenge has only made the system more resilient.”

Question 5. Bitcoin price has been volatile going from $1 to $10,000 back to $3000 to $60000 then to $30000 now to $100000. At what point does the price stabilize and the volatitlity recide. What would need to take place for this to occur and what could the potential price of a single Bitcoin be when it does?

Andreas Antonopoulos: “The volatility we’re seeing is natural for a new monetary asset in its monetization phase. Think of it as Bitcoin’s childhood – it’s growing and maturing. Stability will come with mass adoption and market maturation, likely when Bitcoin’s market cap reaches into the tens of trillions. At that scale, it would take enormous capital to move the price significantly. As for price potential, if Bitcoin becomes a global store of value competing with gold and government bonds, each Bitcoin could be worth millions in today’s dollars. But more importantly, at that stage, we might stop measuring Bitcoin in dollars altogether. The key milestone for stability isn’t a specific price – it’s when Bitcoin achieves sufficient liquidity and market depth across global markets.”

Warren Buffett: “The idea that Bitcoin will somehow ‘stabilize’ fundamentally misunderstands what creates price stability. Stable assets have intrinsic value and generate real cash flows. Bitcoin will always be volatile because its price is purely speculative. Look at gold – even with thousands of years of history and universal recognition, it remains volatile. Bitcoin, which has no inherent value, will be even worse. The only way it would stabilize is if it failed and went to zero. All these price predictions of millions per Bitcoin are exactly the kind of speculation that proves my point – it’s a gambling vehicle, not an investment.”

Milton Friedman: “Price stability in any monetary system comes from broad adoption and deep markets. However, Bitcoin presents a unique case because of its fixed supply schedule. In theory, if Bitcoin achieved widespread adoption as a global store of value or medium of exchange, its price in fiat terms would generally appreciate over time as productivity increases, opposite to how fiat currencies typically depreciate. True price stability might occur when Bitcoin’s market cap reaches that of major fiat currencies, perhaps in the $10-20 trillion range. At that point, with one Bitcoin potentially worth several million dollars, it would take immense capital to create significant volatility.”

Adam Back: “The volatility question is fundamentally about market maturity and liquidity. Currently, Bitcoin’s global liquidity and derivative markets are still developing. Stability will come with institutional adoption, deeper derivative markets, and broader global usage. Given Bitcoin’s fixed supply of 21 million, if it captures even a fraction of global store of value markets (gold, government bonds, real estate), simple math suggests each Bitcoin could be worth millions. The key to reducing volatility is market depth – when daily trading volumes consistently exceed hundreds of billions or trillions of dollars. We’re already seeing this evolution with increasing institutional participation and futures markets. Looking at the stock-to-flow model and historical adoption curves, stability could come within this decade as market cap grows into the trillions.”

Question 6. Looking at Cryptocurrencies more broadly we could see some very high level categories. Bitcoin, Smart Contracts, Stable Coins. How would these three work together and would Bitcoin somehow be an anchor for the other two?

Andreas Antonopoulos: “Bitcoin serves as the foundational layer – the ultimate settlement network and store of value. Smart contract platforms like Ethereum are the programmable layer that enables complex financial applications. Stablecoins bridge the gap between crypto and traditional finance. These layers are complementary, not competitive. Think of Bitcoin as digital gold, providing the hard monetary base that backs the entire crypto economy. Smart contracts enable programmable finance built on top of this base layer, either through Bitcoin’s Lightning Network and Taproot capabilities, or through other blockchains. Stablecoins provide the bridge for day-to-day transactions and business operations. We’ll likely see increased interoperability between these layers through technologies like atomic swaps and state chains, with Bitcoin’s security and network effect anchoring the entire system.”

Warren Buffett: “Adding more complexity to a fundamentally flawed system doesn’t make it better – it makes it more dangerous. These different cryptocurrency categories just create more ways for people to get hurt. Smart contracts? More points of failure and hack vulnerabilities. Stablecoins? We already have stable currencies – they’re called dollars, euros, and yen, backed by actual governments and central banks. This attempt to create an entire parallel financial system is reminiscent of the complex derivatives that led to the 2008 financial crisis. More complexity means more risk, not less.”

Milton Friedman: “The interaction between these three categories represents a fascinating example of spontaneous market organization. Bitcoin could indeed serve as the ‘monetary base’ in this system – similar to how gold once backed national currencies. Smart contracts would function as the commercial banking layer, enabling complex financial arrangements without traditional intermediaries. Stablecoins could act as the medium of exchange layer, similar to how bank notes once represented claims on gold. This three-layer system might actually be more stable than our current financial system because it’s based on a truly limited asset (Bitcoin) rather than infinitely printable fiat currency. The key is that all of this emerges through market forces, not central planning.”

Adam Back: “From a technical perspective, these layers form a natural hierarchy. Bitcoin’s robust security model and proven track record make it the ideal base layer for storing value. Smart contract platforms can either build directly on Bitcoin through solutions like RSK and Lightning, or operate as separate chains with Bitcoin as the primary collateral. Stablecoins, whether algorithmic or fiat-backed, benefit from Bitcoin’s liquidity and market depth as the primary collateral asset. The future likely involves increased technical integration between these layers – imagine Bitcoin-backed stablecoins using advanced smart contracts for decentralized stability mechanisms. The key is that Bitcoin’s unmatched security and decentralization provides the solid foundation that makes the other layers possible.”

Last Question, what does the future hold for Bitcoin and the future of finance?

Andreas Antonopoulos: “What we’re witnessing is not just a new asset class, but a fundamental transformation of money itself. Bitcoin represents the separation of money and state – as significant as the separation of church and state. In the future, we’ll see a world where open, borderless financial systems are the norm. Bitcoin will serve as the foundation for a new financial stack where individuals have true financial sovereignty. The Lightning Network will enable instant, nearly free global transactions. Traditional banks will either adapt or become obsolete. We’ll see the emergence of decentralized financial services accessible to the billions of currently unbanked people. The real revolution isn’t the price of Bitcoin – it’s the democratization of financial access and the end of monetary repression.”

Warren Buffett: “The future of finance will remain firmly rooted in traditional, regulated institutions and government-backed currencies. While technology will certainly improve financial services – making them faster, cheaper, and more accessible – the fundamental need for trusted intermediaries and regulatory oversight won’t disappear. Bitcoin and cryptocurrencies are likely to end up as a cautionary tale, similar to many other financial manias throughout history. The real innovation will come from established financial institutions adopting blockchain technology where it makes sense, while maintaining the security and stability that traditional finance provides.”

Milton Friedman: “The future will likely see a competitive monetary environment where different forms of money compete freely in the marketplace. Bitcoin has initiated a fundamental shift toward private, market-based monetary systems. This competition will force central banks to be more disciplined in their monetary policy, or risk seeing their currencies lose market share to alternatives like Bitcoin. We might see a hybrid system where Bitcoin serves as a global reserve asset while various digital currencies, both private and state-issued, compete for different use cases. This monetary competition would result in better outcomes for citizens globally, as it removes the government monopoly on money that I’ve long criticized.”

Adam Back: “From a technical perspective, we’re moving toward a future where Bitcoin becomes the global settlement layer for value transfer. Layer 2 solutions like Lightning Network will handle everyday transactions, while sidechains and state chains will enable smart contract functionality without compromising Bitcoin’s core security model. We’ll see increased institutionalization with spot ETFs, corporate treasury adoption, and nation-state accumulation. The development of Bitcoin-native financial services will accelerate, potentially replacing much of traditional finance. The key technological challenges around scaling and privacy will be solved through innovations like Taproot, Schnorr signatures, and future improvements. In the long term, Bitcoin could become the world’s primary store of value and settlement layer, with its market cap reaching into the tens of trillions of dollars.”

Key Takeaways

This thought experiment reveals several important insights:

- The Bitcoin panel often reflects different fundamental assumptions about value, money, and the role of financial institutions

- Technical, economic, and traditional financial perspectives each bring valuable insights to the discussion

- The future of Bitcoin and cryptocurrency likely depends on the resolution of both technical and social challenges

- The interaction between traditional finance and crypto-assets continues to evolve

Conclusion

While our simulated panel can’t predict Bitcoin’s future, it highlights the complexity of the issues involved and the importance of considering multiple perspectives. The contrasts between these viewpoints suggest that Bitcoin’s journey will continue to generate significant debate as it evolves.

Whether Bitcoin fulfills its promise as a revolutionary financial technology or proves its critics right remains to be seen. What’s clear is that the conversation around Bitcoin has moved beyond simple dismissal or blind advocacy to a more nuanced discussion of its role in the future of finance.

This blog post was created as a thought experiment using Anthropic’s Claude Sonnet 3.5 LLM (AI) to simulate a discussion between different perspectives on Bitcoin. The responses were generated based on known public statements, writings, and positions of the individuals represented.

{kind=link}